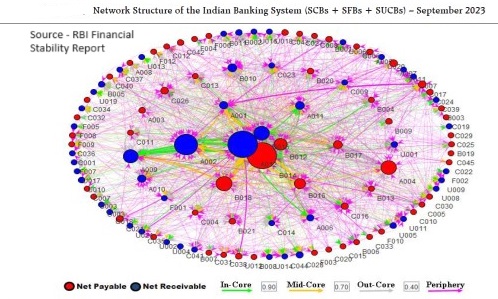

Financial structure of a country is a network of institutions such as Banks, NBFCs, HFCs, Insurance companies, mutual funds and so on. All of these are connected to each other as lenders or borrowers. While the interdependency helps channelize savings into investments, it can also trigger risk events as seen during the global financial crisis […]